Category: Uncategorized

Stewarding our Influence – Part 1

September 10, 2025by Ron Bare

We often hear the phrase, “you don’t need to have power to have influence,” but then struggle to see where that plays out practically. I’d invite you to consider a coworker, past or present, who has a way of quietly encouraging others. They may not have a leadership title, but they bring peace to the workplace and help build a culture of trust, don’t they? Over time, they shape the company’s culture in ways formal leaders sometimes can’t. This is the heart of Christian influence. God entrusts each of us with gifts – relationships, time, and opportunities. How we use those gifts matters, and like that coworker, I hope you are encouraged to leverage your influence, not to make your name great, but to serve God and others.

We all have countless opportunities to steward our influence for God’s kingdom. But how do we know we have been given this role? We read about it in the very first chapter of the Bible! In Genesis 1:28, God says to mankind, “Rule over the fish in the sea and the birds in the sky and over every living creature that moves on the ground.” Then in Genesis 2:15, “The Lord God took the man and put him in the Garden of Eden to work it and take care of it.” In giving mankind authority to “rule” and “take care of” the earth, God demonstrated significant trust. With this trust comes great responsibility. Wherever we engage with this world, at home, the office, our church, or our community, let these passages be a reminder that faithful daily work in these arenas is part of honoring God’s entrusted authority and influence.

Why does this matter? Luke 16:10 reads, “Whoever can be trusted with very little can also be trusted with much…” When we honor God by faithfully engaging our small responsibilities, our influence naturally expands. A small moment of choosing integrity at work, an act of generosity, or a moment of thinking before speaking – all of it shows that we take our responsibilities from God seriously. That small moment of integrity could even evolve into a greater opportunity for influence. Maybe a boss takes note of your integrity. Time after time, integrity proves to be innate in you, and when submitting a name for a promotion, your boss thinks of you. Now, trusted with a supervisory role over other employees, you have even more influence that can be used for good. Be someone who is trustworthy with little.

Genesis speaks to the fact that we certainly have influence, because of the gifts God has trusted us with. But there’s a parable in Matthew 25 that speaks to the idea of what exactly we should be doing with this influence. The master in this parable entrusts resources, or talents, to three servants. The master leaves for a time and upon his return, finds that two servants invested the talents and multiplied what was given to them, while the third buried the talent, preserving its worth. The master is pleased with the first two servants but condemns the third, going so far as to call him “wicked.” Our influence is just like those talents. Given to us by our master, God, we are reminded that He expects growth, not simply preservation. How are you growing your influence? Today we looked at influence from a 30,000 foot view. Next month, we’re going to come down into the weeds. We hope you’ll consider joining us in October, as we talk about practical ways to steward our influence.

Is it Biblical to Bring Increase to Wealth?

July 31, 2025

by Ron Bare

The idea of increasing wealth can feel uncomfortable or even taboo in many Christian circles – often raising questions about intent, motive, and faith. While conversations about this topic can feel challenging, I invite you to join me in exploring a new perspective today, one that’s deeply rooted in Scripture.

In Matthew 25, Jesus tells a story of three servants entrusted with their master’s resources. The first two servants multiplied what was given to them, and the third servant buried his out of fear. The master praised the first two servants and condemned the third. The difference? Their stewardship of the wealth that was entrusted to them.

Throughout the Bible, we see an ongoing invitation to growth – in faith, love, generosity, influence, and sometimes in wealth. This is not about amassing wealth, but rather about faithful stewardship of the resources God has given to us. Like the third servant, we can become scared to pursue growth, fearing failure or loss. Yet we know that fear is not from God and it should not hold us back from pursuing growth.

Why is it important to consider growing, or increasing, our wealth? Ultimately, we know and trust that God is the owner of all that we have. When done with the right motive, seeking financial growth can be an act of worship as we continue to trust in Him for each of our needs. This principle is clear in Matthew 25 – the master entrusts bags of gold to the servants. The servants did not find the bags of gold on their own; they were given them. What they did with these bags of gold was a reflection of their relationship with their master.

Still, we know this topic can carry a stigma, and many churches shy away from teaching this. Why? The idea of growing wealth can appear similar to the prosperity gospel, the teaching that financial blessing will find you if you are faithful to God or have “enough” faith. The prosperity gospel misrepresents both God’s heart and our calling. Rather, our belief is that God has entrusted us each with specific blessings, and that someday, He will ask for an account of our stewardship. In light of this, we believe stewarding these resources well, including pursuing an increase, can be honoring to God.

But don’t forget the point – this isn’t about chasing wealth. In Psalm 24:1, we see that God is the owner of all things. In Psalm 8 and Genesis 1-2, we learn that though God has created everything, He has put us in charge of His creation. He has asked us to manage and grow the things He has made! If you are blessed to see an increase, what you do with that increase can be a beautiful reflection of your relationship with God. When we can combine this increase with a content heart, a generous spirit, and a purposeful plan, we can impact the Kingdom of God for good. This principle of bringing an increase to our wealth, and all that we have, is a thread that runs throughout Scripture. That’s why our impact statement here at Bare talks about how “intentional stewardship and extravagant generosity can change the world for the glory of God.” How can you change the world through stewardship and generosity? We encourage you to consider how pursuing growth might fit into your story, not for your sake, but for God’s glory.

Letting God “Increase” Our Time

June 26, 2025

by Kurtis Eby

Have you ever thought about how time tends to be experienced uniquely, varying by individual? A child perceives time standing still while on a road trip, but an artist caught in their work blinks, and hours have passed. Though our interactions with time vary significantly, time is uniform at its core. 1 Chronicles 29:11 reminds us that everything in the heavens and the earth is the Lord’s. In Genesis 1:14-19, God created the sun, moon, day, and night – we know that time is from the Lord, too!

He invites us to number our days, knowing that time on this earth is fleeting. But why do we experience time so differently? We tend to view time as being spent rather than being invested. This is understandable, as we live within a 24-hour system that is effective for the use of commerce and community, but what if we lived like God truly was the author of time?

Believing in God for additional resources is commonplace in Christian culture. Time and time again, He proves Himself faithful to supply all of our needs. What other areas might He be inviting us to rely on Him for an increase? What could it mean if we believed in Him for additional time, beyond just talent and treasure? What if He allowed us more effective time? Though this blog wasn’t in our plans, we believe that our theme this year, Year of Increase, relates closely to time. We trust that God can help us invest and redeem time for His glory.

Since God created time, He is not bound by it. In Joshua 10, God caused the sun to stand still. He shifted time to allow for His kingdom to advance. This story reminds us of the truth about God – that He is the author and creator of time. Rather than viewing time as scarce and limiting, we can trust that He has the authority to multiply and increase time.

Consider how partnering with Him in this area could influence our approach to time. What investments do we make in time? When we know what He has given to us and walk in authority in that, I believe He can redeem time. When we are plugged into the source of time, we lack nothing. If we take a moment to analyze our time investment, our core values, and our resources, we just might begin to see how He would have us shift our investments.

I’ve found a simple question that can aid in an evaluation of your time: What does the way that I spend my time tell me about what I love? Take a moment to write out your schedule for the week. What is on your to-do list? Is there room to adjust if a relational opportunity with a neighbor or friend arises? What captures your heart and mind in your spare time? When we say we love our neighbor, but every day of the week is filled to the brim with work, sports games, and house chores, do we really love our neighbor? Or might our time suggest that we love something else a little bit more?

Whether it means canceling plans to accept a service opportunity, designating time each month to give to the church, or something else entirely, we invite you to join us in asking God how our time can be invested. What a joy it is to be able to partner with God to redeem and see an increase in our time.

And please – before you get to feeling that time is just too limited – remember that you, yes YOU, have access to the creator of time!

Bringing an “Increase” Mindset to Our Work

May 19, 2025by Ron Bare

This year, we’ve declared a theme: Year of Increase. We believe that God has entrusted each of us with resources, gifts, and talents, and it’s our responsibility to steward and increase them for His glory. Four important components of increase that we are focused on bringing an “increase mindset” to are: vision, work, wealth, and influence. We believe as our mindset in these areas grows (increases) we are fulfilling our God given purpose and capacity to serve those around us.

When we consider bringing an increase to areas of our lives, it’s only natural that work would be one of those areas. Work dominates a significant portion of our lives, and growth in this area is both normal and expected. Whether your business expands, you receive a promotion, or you acquire a new property, it is likely that you will experience growth within your work. Believe it or not, the Bible has a lot to say about work, this thing that we spend so many years of our lives doing!

Even God worked as He created the world. In Genesis, God describes His work as ‘good’ seven times. God’s greatest work was creating man and woman, in His image. When we consider that God worked, it should be no surprise that work is also a major part of our lives. In Genesis 2:15, God gives Adam and Eve this direction to work: “Then the LORD God took the man and put him into the garden of Eden to cultivate it and keep it.”

These instructions to “cultivate and keep” the garden assume that there is something to be done, or kept up with, or improved. The direction to “cultivate” insinuates development. It suggests that Adam and Eve should spend time discovering the potential of the land and the resources they were given, and bring forth abundance! This direction is not only for Adam and Eve, but for all of humanity. How do we view our own work? Do we consider the potential that our work has and what it could become? What is our vision for the work that we do? God encourages Adam and Eve not to just simply get by and live passively in the garden, but to actively invest in their resources and improve what they were given. Though this can feel like a strong, challenging command, it’s a gift that God allows us to create and improve what He has made. Creation is what God made out of nothing, but culture is what humans get to make out of God’s good creation.

Now, it’s not all so simple. The fall of man has made all of this just a little bit trickier. Because of the fall, work is hard and frustrating at times for many of us. When we dedicate years of our life to work and it becomes difficult, our goal becomes saving enough so that we will be able to stop working, or retire. Though retirement from a job or full time work may be appropriate, working for a lifetime with the sole purpose of retiring is not biblical.

Instead, work should be a blessing! Through our work, we get to join in partnership with God to create and improve the earth. We get to influence culture to see God’s good creation through the goods and services we provide. What a gift! The way that we view work should, and likely will change as we get older. However, the challenge is to never stop asking this key question: “What work does God have for me with the gifts, abilities, and experiences He has given to me?” For as long as we have breath, let that be our heart’s cry!

We believe that having an ‘increase’ mindset around work can be so impactful. It allows us to consider what things God has gifted us with and how He might have us use them. Our job is to take what He has given us, improve the earth, produce more goods and services that benefit humanity, and create a culture that brings His kingdom on earth as it is in Heaven.

If you’re interested in more resources relating to this topic, check out these books:

Every Good Endeavor by Tim Keller

Sacredness of Secular Work by Jordan Raynor

Garden City by John Mark Comer

Planning for Uncertainty

April 24, 2025by Ron Bare

Early in my career I remember hearing that it is wise to plan for the “Certainty of Uncertainty”. As a financial advisor, this really resonated with me. Reflecting on that phrase now, after 30 years of experience, including various times of uncertainty, I firmly believe in the truth of that wisdom. When economic or market uncertainty is elevated, we believe in the importance of going back to values and principles to help you make wise financial decisions. And here at Bare Wealth Advisors, we believe the best values and principles to apply are those that are grounded in Biblical wisdom. Here are a few to consider during times of greater uncertainty:

- Think Long-Term. A long-term perspective is very important to consider when thinking about investment decisions. The longer your perspective is, the better financial decisions you will typically make. Investing in the ownership of companies (which is what you do when you invest in the stock market) carries risks of economic and financial events. When you step back and look at the long term, investors are often rewarded for the risks taken. (Proverbs 13:11, 28:19-20)

- Diversify your investments. In our planning process we intentionally build our portfolios across various industries, sizes of companies and countries to help ensure diversification. We use various professional managers with many years of experience. In addition, we typically hold 5+ years of cash needs (or income) in more conservative investments that are not subject to as much market volatility in the short term. This allows investors to apply principle #1 – think long-term. (Ecclesiastes 11:1-2)

- Minimize debt. When a company or individual has minimal debt levels it reduces risks to their overall plan and future when uncertainty happens. (Proverbs 22:7, 26-27)

- Increase Generosity. We talk a lot about generosity at Bare. We believe being generous is one of the most important biblical principles to apply to our finances. Generosity takes a step of faith, it helps us to learn to trust God and be grateful. When we live with open hands and are generous to those in need, we are reminded of how blessed we are. Times of uncertainty are great times to consider how to be a blessing to others. (1 Timothy 6:17-19, 2 Cor. 9)

- Increase Margin. Financial margin can be vastly underrated. When you have margin in your monthly income and margin on your balance sheet it gives you a chance to take advantage of market volatility. Most people have heard the phrase “buy low – sell high,” but many are not prepared with margin to implement this when opportunity arises. (Proverbs 6:6-8). A good way to increase margin is to live within a budget to ensure that you have excess money to save and invest each month. Additionally, it is helpful to hold some cash in a reserve account for unexpected expenses as well as unexpected opportunities.

As always, we are here to talk to you about your personal financial and investment plans. We care about you and your family and remain committed to helping you steward your resources according to your God-given purpose; assisting you to make a significant difference in this world! I will leave you with a few quotes from two famous and successful investors:

Warren Buffet – “If you aren’t willing to own a stock for 10 years, don’t even think about owing it for 10 minutes”

John Templeton – the four most dangerous words for an investor “This time is different”

Staying the Course During Market Volatility

April 8, 2025by Ron Bare

Along with most Americans, we’ve been watching closely as President Donald Trump declared April 2nd to be “Liberation Day” and implemented broader tariffs than anticipated by economic watchdogs and television pundits. These tariffs, which include a 10% duty on all imports to the U.S. and meaningfully higher rates for some countries in particular, have had an immediate negative impact on the markets and led to concerns about a potential recession and increased market instability.

As always in times of such volatility, it’s natural to feel anxious about your investments. The rapid swings in stock prices can stir emotions, but it’s essential to remember that historically markets have demonstrated resilience over the long term, even in the face of policy-induced volatility.

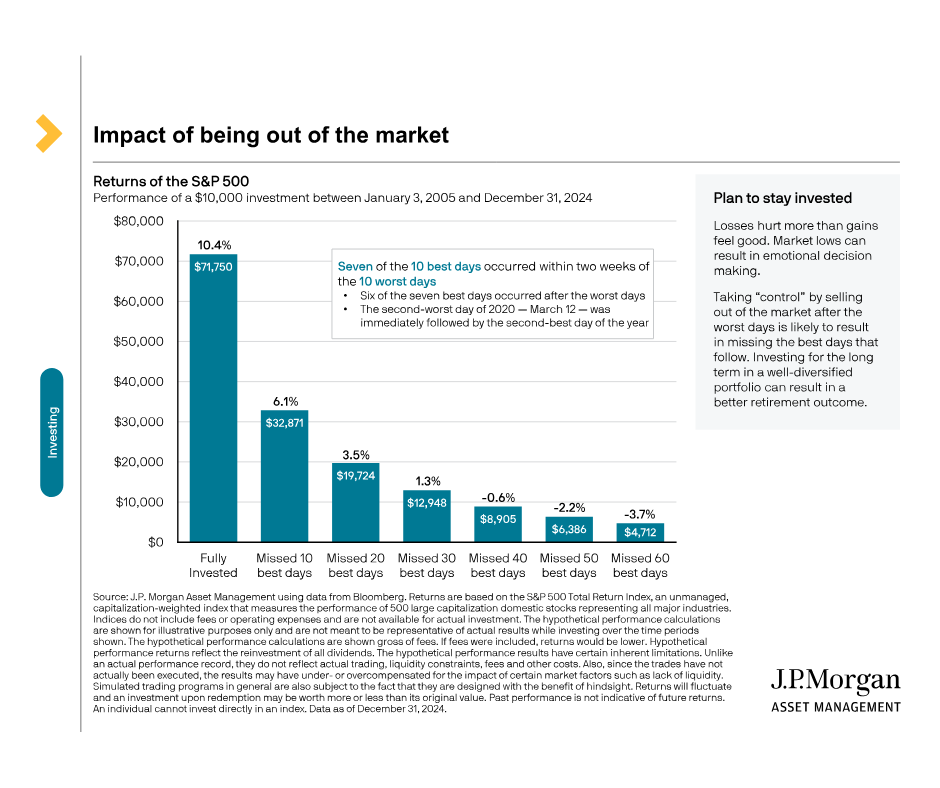

J.P. Morgan Asset Management’s oft-quoted research illustrates the importance of staying invested through turbulent periods. In one study, they analyzed the performance of a $10,000 investment in the S&P 500 between January 2004 and December 2023. If the investor stayed fully invested, the average annual return was 10.4%. However, missing just the 10 best days during that period cut the return to 6.1%. Missing the 20 best days dropped it further to 3.5% (see the data here). The impact of being out of the market for even a few key days—most of which tend to occur during periods of heightened volatility—can be dramatic.

“The stock market is a device for transferring money from the impatient to the patient” – Warren Buffett.

As the ‘Oracle of Omaha’ reminds us in the above quote, it’s important to keep in mind the psychological impact of market volatility. Behavioral finance studies suggest that the pain of losses often feels more intense than the pleasure of gains—a concept known as loss aversion. This can lead to panic selling, which often locks in losses and prevents investors from participating in subsequent market recoveries. Staying focused on your long-term goals and resisting the urge to make hasty decisions can help you avoid these pitfalls.

While this is the largest wave of American tariffs since President Hoover signed the Smoot-Hawley Tariff Act in 1930, it’s essential for us to maintain a long-term perspective. Reacting in fear or attempting to time the market during such periods can lead to missed opportunities and diminished returns. By staying the course and focusing on your long-term investment objectives, you position yourself to navigate through this volatility more effectively. Please see below for helpful graphic information on the value of staying the course.

As always, our team is here to support you in aligning your investment strategy with your financial goals, helping you navigate these uncertain times. Be on the lookout for additional communications and resources from our office in the coming days. In the meantime, we are available to talk if you’d like to reach out and discuss anything on your mind.

Helping You Plan Well for Retirement

March 19, 2025

by Adam Black

Retirement is a significant milestone in American culture – a chance to reflect on your life’s journey and accomplishments. As you reflect, looking back in the rear view mirror of your life, what do you hope to see?

This year at Bare, our theme is Year of Increase. We believe in helping you expand your vision for all that you’ve been entrusted to steward. Many of us understand the call to steward our resources, but Matthew 25 reminds us of the call to also increase what we have been given! How can we plan well for retirement and increase our resources, so that we can serve our families and communities?

Planning for retirement can feel overwhelming, but taking time to make informed decisions is the key to being set up for a secure future. Inviting a financial advisor into this process can help make the process smoother. Today, we’ll answer 3 common retirement questions, to help us all approach retirement with confidence, clarity, and a vision for increase.

- At what age should I take my Social Security?

Social Security has been a hot topic in the news recently! I’ll be the first to admit that I don’t know what will happen with it over the coming years. What I do know is that it can play a large role in any retirement plan. When is the best time to take Social Security? It varies, but before a decision can be made, it’s important to understand some of the rules.

Social Security can be taken as early as age 62. It is important to note, however, that taking Social Security at 62 will result in a reduction of your Full Retirement Age benefit for the rest of your life. Full Retirement Age for most people today is age 67, which is when you are entitled to your full benefit. The latest age that Social Security can be taken is age 70. For each year that you delay your benefit from Full Retirement Age until age 70, you will get an 8% increase on your benefit for the rest of your life as long as you were born after 1943.

If you plan on retiring on the earlier side, it may make sense to take your Social Security benefit, but if you never plan on slowing down (I’m looking at you, farmers), it may make sense to get the largest possible benefit by waiting until 70. If you have a family history of health concerns, you may want to collect earlier to get benefits for more years, but if you plan to live until 100, you will receive more money over your lifetime by delaying. Everyone’s financial, health, and retirement goals are different, so inviting a trusted financial advisor into this process can help you maximize your Social Security benefits.

- What do I do about health insurance?

For those retiring at 65 or later, Medicare most likely is the answer. After all, you have been paying into it for nearly all of your working life – you might as well take advantage of it! Medicare is made up of a few parts that each serve different purposes.

Medicare Part A is hospital insurance. It covers inpatient hospital stays, skilled nursing facility care, hospice care, and some home health services. Most people don’t pay a premium for Part A because they paid Medicare taxes while working.

Medicare Part B is medical insurance. Part B covers outpatient services, including doctor visits, preventative care, lab tests, outpatient surgeries, and some home health care. The monthly premium is taken directly from your Social Security benefit if you are collecting. Most people do pay deductibles and copays for services.

Medicare Part C, or Medicare Advantage, are private plans that offer all the benefits of Parts A and B, and additional services (dental, vision, hearing, etc.). Medicare Advantage plans usually include prescription drug coverage and have out-of-pocket cost limits, so it could be a more advantageous health coverage option for you.

Medicare Part D helps cover the cost of prescription medications, either through stand-alone prescription drug plans or as part of a Medicare Advantage plan.

Finally, Medicare Supplement Insurance, or Medigap, helps pay for out-of-pocket costs like copayments, coinsurance, and deductibles.

- Are my investments protected?

It’s understandable that retirees may worry whether their hard-earned nest egg will lose value, especially when they have no plans to return to work. Any investment outside of cash or an FDIC-insured product like a CD does carry some risk. Yet if all of your investments were cash, they would likely be beat out by the cost of living. So how can you ensure that your money is protected for short-term needs, while making sure it outpaces inflation and lasts a lifetime?

One of our favorite approaches is ‘segment planning,’ which involves defining how much is enough for you in each phase. The first phase aims to protect money from loss of principle that you need in the short term (roughly the next 5 years) by using products like cash and CDs. After this segment is filled, we plan for segment two which are years 6 – 10. For this segment, we often use investment products like fixed annuities or bonds. In segment three, which are years 11+, we look to outpace inflation with higher risk investments that offer a higher growth potential. These investments might include stocks, real estate investments, or growth-focused mutual funds and ETFs. We have seen the stock market grow in most 10-year windows, which gives us confidence to move forward. Even if a segment decreases in value in year one, there is time for it to recover. As you progress, funds from later segments move into the adjacent segment, ensuring that the next few years of necessary funds are available and as close to risk-free as we can get.

There’s a lot to consider in retirement, and I’m sure that this blog raised questions that I couldn’t address today. Retirement planning is a serious endeavor, and many people underestimate how impactful it can be to work with a trusted advisor. I often hear, “I wish I would’ve met with an advisor sooner,” but the key is that they are meeting with one now, instead of 10 years from now. I’d encourage all upcoming retirees to find an advisor who is trustworthy, aligns with your values, and has your best interest in mind. They will help give you confidence to step into retirement, whenever the Lord calls you into that season.

Year of Increase – Creating a Vision for our Resources

February 10, 2025

by Ron Bare

Have you ever met a visionary? Maybe you’re one yourself. I’m talking about that person who seems to have endless ideas, always sees the big picture, and is always trying to fit 100 pounds into a 50-pound bag. Though our visionary friends do have some drawbacks, I’m convinced they bring something to the table that each of us can learn from.

This valuable trait that visionaries have is simply having a vision and being able to look beyond the current moment. Here at Bare, we often refer to our vision as “Beyond Abundance.” When we look down the road 5, 20, or 50 years into the future, what we hope for our clients is not that they’ve become rich, but that they’ve lived a rich and full life. We pray that our clients have been blessed beyond their basic needs, and that they have served others with their abundance. We also pray that our clients have taken a good, long look at their resources and considered how they might bring an increase to them for the good of others.

How can we ensure that at the end of our life, we’ve done this well? Investing and growing our finances, time, and resources is no small feat, but it is worth it! Ephesians 3:20 and 2 Corinthians 9 both remind us of this reality – that when we sow, we reap. As you take a look at your life, what has God placed in your hands? How can you invest and grow the resources that God has given to you? What kind of impact can your resources have on others?

We can talk about these principles all day, but it’s crucial to take time to nail down what this actually looks like in your life. We want to intentionally create a vision for our resources, and vision first begins with inventory. To aid in this process, we’ve crafted the Beyond Abundance Inventory Sheet. This tool helps us think about exactly what resources God has given to us and how we can bring an increase to them for His glory.

The first resource on the inventory sheet is our financial resources. Whether a salary, an inheritance, or ownership of a business, financial resources are easy to see. After we know what financial resources we have, we can consider giving, investing, or planning how our business can serve others. These resources are so tangible, but certainly not all there is.

Intellectual resources might include a high school or college education. They might include a specific skill that you are trained in, or unique experience that you have. They may even include financial literacy. These are the kinds of gifts that are important to continue investing in, and as learning continues, are important to pass on to others through teaching and apprenticeship.

Relational or social resources come in the form of people. You’ve heard it said before: who you know is often more important than what you know. Many of you know this principle to be true because you’ve lived it. One of my favorite ways to watch networks serve the community is through banding together to solve a problem. Often, one person or organization does not have all of the solutions to a problem, but when networks work together, things get done. How can you work with others to solve big problems?

We also believe spiritual resources are critical. It is such a gift to be able to live in a time and place in history where spiritual resources are easy to access – whether a church, pastor, or our Bible. Going one step further and inviting others to join in is where true transformation happens.

The last category on the Beyond Abundance Inventory Sheet is physical resources. This includes those tangible things – housing, food, and clothing. Though many of us are blessed, many of our neighbors are under-resourced in this area. How can we use our physical resources to come alongside them? Whether buying properties and renting them at fair rates or donating food to food banks, there are plenty of ways to serve.

At Bare, we believe that stewardship and generosity are important. That’s why our impact statement highlights these two ideas: through intentional stewardship and extravagant generosity, we help generous people shift the culture and change the world for the glory of God. Would you join us on this mission? We’d love to have you!

Exploring Biblical “Increase” in 2025

January 10, 2025

by Ron Bare

Each year at Bare, we choose a theme to focus on that guides us both internally and externally. As we considered the theme for 2025, we chose “year of increase.” At first glance, it may seem practical for a wealth advising firm to have a focus on increase. However, this year is not about increasing wealth for the purpose of becoming wealthy, but rather for the purpose of increasing our influence. Our culture tells us that we will ‘win’ if we can grow our wealth, get the highest rate of return, or show a higher net worth statement at the end of each year. Yet this cultural view falls short of the Biblical view of success, influence and increase.

The Biblical view of bringing an increase to what we have been given draws us to look at two places – the origin of life in Genesis, and a parable in Matthew 25. In these passages, we see that growing and increasing the things God has entrusted to us is an important piece of stewardship. Does this exclusively refer to money? Is bringing an increase in all areas even within our control?

We have found that a great way to explore these questions is to start at the beginning – the very beginning. In Genesis, we see God’s final and most stunning creation: humanity. He created human beings and gave them a few instructions: to multiply, fill the earth, govern the earth, and rule. He gave it all to humans and said, ‘it is yours!’ This can easily be a passing thought, but when we stop to reflect on what God has done, we are reminded of the incredible gift – not just to enjoy creation, but also to steward it! (also read Ps. 8, Gen. 1 and 2, and Matt. 25). I don’t know about you, but I’m not sure I’d want to hand over the keys to my creation to someone else!

God has given over His creation to us for the time being, and much like the master in the parable, He will return to see what we have done with it. In the parable in Matthew 25, both servants who increased what had been given to them were praised, while the one who buried it in the ground was punished.

Readers of this story tend to react through one of two extremes, neither of which we ascribe to. One extreme is the reader who believes that God will always bless them exponentially, and that if they just trust Him, wealth is not far behind. The other extreme is the reader who is filled with fear, like the final servant in the parable. This person is afraid of risk and afraid of losing what was given to them, so they do nothing with their assets. This person doesn’t work, invest, or give.

Unlike the person enamored with the prosperity gospel and certainly unlike the fearful servant, we want to focus on increasing our resources for the glory of God, so that we can give, serve, and shape culture. Our tagline at Bare is “Beyond Abundance,” and we believe it helps us carry a vision beyond simply amassing wealth. Instead, it is centered around influencing the world for good. Living “beyond abundance” assumes a confidence in God, acknowledging that He can richly provide for us beyond what we need, so that we can generously share with others. A “beyond abundance” way of living offers freedom and opportunities to live a life of fullness, and to impact the world far beyond what we could do on our own.

In 2025, we will explore together what it means to steward all that God has given to us to carry out these instructions. Stewardship is first an understanding that we are not the owners but rather the managers of what we have (earth, wealth, time, talents, etc.) and secondarily an understanding of the responsibilities that come from the owner (God). We will focus on four key areas this year – our vision, our work, our wealth, and our influence. Join us as we consider how intentional stewardship and extravagant generosity can impact the world to be just as it was originally intended – an environment where humans can flourish.

Passing on Biblical Wisdom to the Next Generation

November 1, 2024

By Ron Bare

While stopped at a red light today, the image on the box truck in front of me caught my eye. There, displayed on the back of the truck, was an image of a family enjoying a meal together. All of a sudden, I found myself craving a delicious holiday meal. (Thankfully, those meals are just around the corner.) Even more than those meals, I found myself craving quality family time. That advertisement was sure doing its job! The holidays are a beautiful time to spend time with those you love most, and I hope you get to enjoy the gift of family in just a few weeks.

Not only are the holidays filled with food and family time, but they’re also filled with conversation. What topics of conversation typically fill your table during the holidays? Our conversations often revolve around life updates, stories from work, excitement for the new year, and family memories. As I look ahead to the holidays this year, I wonder if there’s a new topic of conversation we could, and perhaps should, bring to the table.

What would it look like to start intentionally passing on wisdom to our families? I truly believe that passing on wisdom to the next generation is one of the best ways to be faithful with what we have been given. It is a beautiful opportunity to leave a lasting legacy. When those we love can learn from our mistakes without having to make the mistake themselves, it saves time and lowers stress. It allows for room for them to make their own mistakes and grow, while acknowledging the wisdom you’ve already passed on to them.

Wisdom is a common topic throughout the Bible, especially in Proverbs. In Proverbs 2, we read about how to obtain wisdom and how wisdom changes us. Verse 6 reads, “For the Lord gives wisdom.” Where else could it come from? Who else knows all? I am encouraged when I remember that we have direct access to the Lord and can ask Him for wisdom through prayer. Let us rejoice that our God offers us this gift!

When the Lord does graciously choose to grant us wisdom, we see its impact permeate our lives. When we have wisdom, we fear the Lord. When we have wisdom, we gain knowledge that can only come from God himself. He guides us as we live and grants us a sense of right and wrong. Wisdom acts as a shield and a protection from things that we may not have otherwise been aware of, including evil or immoral things.

As we grow older and experience more of life, we tend to grow in wisdom. Each success and failure have something to teach us. With every experience, we gain more wisdom that can be passed on. The Lord has granted these opportunities to us, and I believe that sharing these experiences and wisdom with our children and grandchildren is both an incredible opportunity and responsibility.

As we enter the final months of this year, consider bringing a new topic of conversation to your table. What wisdom can you bestow upon those you love? It might be as simple as asking a few questions. Ask someone in your family, “What is something you have learned this year?” Consider powerful stories from the last few months or years that have shaped your thinking, your principles, and your beliefs. Be prepared to share these things with your family as you share meals together.

Many biblical men and women have prayed for wisdom throughout the years. We look to Moses, whose prayer we hope is the echo of each of our hearts: “Heavenly Father, teach me to number my days that I may gain a heart of wisdom.” I pray that this holiday season, we each desire to both grow in wisdom and share it with those we love.